Everything You Need to Know About Stamp Duty in 2025

Stamp Duty Land Tax (SDLT) is a levy imposed on the purchase of property or land when the transaction value exceeds a specific threshold in England and Northern Ireland. This guide will focus on the regulations applicable in England for residential properties in 2025, as property transaction taxes operate differently in Scotland (Land and Buildings Transaction Tax) and Wales (Land Transaction Tax), each with its own set of rates and thresholds. Whether you are buying a freehold or leasehold property, with or without a mortgage, understanding the SDLT rules is crucial, especially with legislative changes on the horizon for 2025.

Standard Stamp Duty Rates and Thresholds for Residential Properties

The standard SDLT rates for residential property purchases in England are set to change from 1st April 2025. These rates apply to individuals buying a property who will own only that one residential property after the purchase.

A significant change taking effect in April 2025 is the reduction of the initial threshold at which SDLT becomes payable. Currently, until 31st March 2025, this nil-rate band extends up to £250,000. The halving of this threshold to £125,000 means that individuals purchasing properties priced between £125,001 and £250,000 will now incur a 2% SDLT on that portion of the value. This adjustment will likely increase the upfront costs for many homebuyers in this price range.

To illustrate how SDLT is calculated, consider a property purchased for £300,000 from April 2025 onwards. The calculation would be as follows: 0% on the first £125,000 (£0), 2% on the next £125,000 (£125,001 - £250,000), which amounts to £2,500, and 5% on the remaining £50,000 (£250,001 - £300,000), totaling £2,500. Therefore, the total SDLT payable would be £5,000. This example demonstrates the progressive nature of SDLT, where different segments of the property's value are taxed at increasing rates. This system ensures that higher-value properties attract a greater proportion of tax.

Stamp Duty Relief for First-Time Buyers

First-time buyers in England can benefit from a specific SDLT relief, provided that they and anyone they are buying with have never previously owned a property, either in the UK or elsewhere in the world. The rules for this relief are also changing from 1st April 2025.

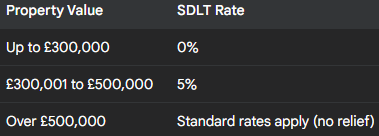

Currently, until 31st March 2025, first-time buyers paid no SDLT on properties up to £425,000, with a reduced rate of 5% on the portion between £425,001 and £625,000. From April 2025, the threshold for paying no SDLT will decrease to £300,000, and the 5% rate will apply to the portion between £300,001 and £500,000. Furthermore, the maximum property value for which first-time buyer relief can be claimed is also being lowered from £625,000 to £500,000. These changes suggest that while first-time buyers still receive a benefit, it will be less generous for those purchasing properties in the upper end of the first-time buyer market.

Consider a first-time buyer purchasing a property for £400,000 in April 2025. They would pay 0% on the first £300,000 and 5% on the remaining £100,000 (£300,001 - £400,000), resulting in a total SDLT of £5,000. Comparing this to the standard rate calculation for a £300,000 property (£5,000), it highlights that first-time buyers still gain an advantage by avoiding tax on the initial £300,000. However, the reduction in thresholds means that more first-time buyers might find themselves paying some level of SDLT compared to the rules in place before April 2025.

Higher Stamp Duty Rates for Additional Residential Properties (2025)

Higher rates of SDLT typically apply when an individual purchases a new residential property that results in them owning more than one. This includes the purchase of second homes and buy-to-let properties. It's important to note that these rules extend beyond the individual buyer and also apply to their spouse or civil partner and anyone else they are purchasing the property with.

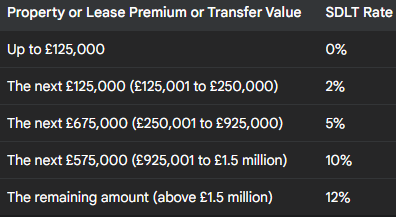

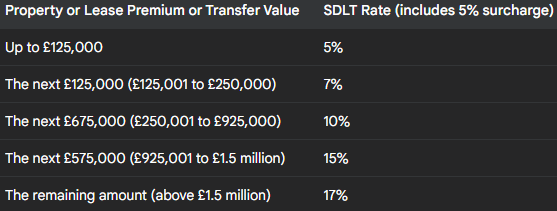

The higher SDLT rates applicable from 1st April 2025, which include a 5% surcharge, are as follows:

A notable change is the increase in the surcharge for additional properties from 3% to 5%, which took effect on 31st October 2024. This increase will significantly raise the cost of purchasing additional residential properties. The government's rationale behind this adjustment is likely to influence the buy-to-let market and potentially increase the availability of properties for first-time buyers and owner-occupiers.

However, the higher rates might not apply if the new property is replacing your main residence and your previous main residence was sold within 36 months of completing the new purchase. If you haven't sold your previous main residence by the time you complete the purchase of the new one, you will initially pay the higher rates but may be eligible for a refund if the sale is completed within the 36-month timeframe.

For example, consider the SDLT payable on a £300,000 buy-to-let property purchased from April 2025. The calculation would be: 5% on the first £125,000 (£6,250), 7% on the next £125,000 (£125,001 - £250,000) which is £8,750, and 10% on the remaining £50,000 (£250,001 - £300,000), totaling £5,000. The total SDLT would be £20,000. This is considerably higher than the £5,000 payable at the standard rate for the same property value, highlighting the significant financial impact of the higher rates for additional property purchases.

Anticipated Changes and Updates to Stamp Duty Legislation in 2025

The most significant legislative change for SDLT in 2025 is the end of the temporary higher thresholds that were introduced in September 2022. These temporary measures will expire on 31st March 2025, and from 1st April 2025, the SDLT rates and thresholds will revert to the levels detailed in the previous sections. This means that the period leading up to 31st March 2025 offers a potential advantage for buyers of main residences (where the nil-rate threshold is currently £250,000) and first-time buyers (where the nil-rate threshold is £425,000). Completing property transactions before this deadline could result in lower SDLT liabilities for some buyers.

Additionally, as mentioned earlier, the surcharge for purchasing additional residential properties increased to 5% on 31st October 2024. At present, no other significant changes to SDLT legislation for 2025 have been officially announced in the provided information. However, it is always prudent to consult official government sources for the most current information as the year progresses.

How is Stamp Duty Calculated in 2025?

SDLT is calculated using a 'slice' or 'band' system. This means that the tax rate varies depending on the portion of the property purchase price that falls within each tax band. To calculate the SDLT payable:

- Determine the total purchase price of the property.

- Identify your buyer status (e.g., first-time buyer, standard buyer, additional property owner).

- Consult the relevant tax rate table for your status and the applicable period (from April 2025).

- Apply the corresponding tax rate to each segment of the property value that falls within each threshold.

- Sum the tax amounts for each segment to arrive at the total SDLT liability.

The buyer's status is a critical factor in determining the applicable rates and thresholds. As demonstrated in the previous examples, the SDLT liability can differ significantly based on whether the buyer is a first-time buyer, a standard homebuyer, or purchasing an additional property. The example of a £300,000 standard purchase, where the tax is calculated across different price bands at varying rates, clearly illustrates this 'slice' system in action.

Stamp Duty Exemptions and Reliefs

Beyond the first-time buyer relief, there are other specific circumstances where SDLT might not be payable or where other reliefs could apply. These include situations such as:

- When property is left to someone in a will.

- When property is transferred due to divorce or the dissolution of a civil partnership.

- When a freehold property is bought for less than £40,000.

- For certain new leasehold purchases where the premium is below £40,000 and the annual rent is less than £1,000, or for assigned leases of less than 7 years where the amount paid is below the residential threshold.

- When properties are purchased by charities for charitable purposes.

- Various other reliefs exist for specific buyers or transactions, such as building companies buying an individual’s home, employers buying an employee’s house, local councils making compulsory purchases, property developers providing amenities, companies transferring property to another company, right to buy properties, registered providers of social housing, Crown employees, and property investment funds.

The existence of these diverse exemptions and reliefs indicates that SDLT regulations can be nuanced, and individuals in specific situations should always investigate their eligibility to potentially reduce or avoid SDLT. These provisions often cater to particular types of transactions or buyers with defined statuses, highlighting the fact that SDLT is not universally applied in the same manner.

It's also important to remember the 2% surcharge that applies to non-UK residents purchasing residential property in England and Northern Ireland, which is added on top of any other applicable SDLT rates.

Official Stamp Duty Calculators and Guidance from the UK Government

For the most accurate and up-to-date information on SDLT, it is essential to consult official UK government websites. Here are some useful links:

- Main GOV.UK page for Stamp Duty Land Tax: https://www.gov.uk/stamp-duty-land-tax

- Residential property rates: https://www.gov.uk/stamp-duty-land-tax/residential-property-rates

- SDLT calculator (via MoneyHelper): https://www.moneyhelper.org.uk/en/homes/buying-a-home/stamp-duty-calculator

- Guidance on buying an additional residential property: https://www.gov.uk/guidance/stamp-duty-land-tax-buying-an-additional-residential-property

- Information on reliefs and exemptions: https://www.gov.uk/stamp-duty-land-tax/reliefs-and-exemptions

The provision of official online tools and information by the government highlights their effort to make complex tax regulations more accessible to the public. Prospective homebuyers should utilize these resources to obtain personalized SDLT estimates and remain informed about the latest rules and any potential updates.

Conclusion: Key Considerations for Stamp Duty in 2025

In summary, the Stamp Duty Land Tax landscape in England is set to undergo notable changes in 2025. The reversion to previous nil-rate thresholds in April will impact both standard homebuyers and first-time buyers, potentially increasing the initial costs of purchasing property, particularly in the £125,001 to £250,000 price range. First-time buyers will continue to benefit from relief, but the thresholds for this relief are also being reduced. The significant increase in the surcharge for additional residential properties, effective from October 2024, will make buy-to-let investments and second home purchases more expensive.

These changes will affect different types of buyers in varying ways. First-time buyers looking at properties between £300,001 and £425,000 will face a new SDLT liability, while those purchasing properties between £125,001 and £250,000 will now pay SDLT where they might not have under the temporary thresholds. Investors and second homeowners will need to factor in the increased 5% surcharge, significantly impacting their returns.

It is crucial for anyone planning to buy property in England in 2025 to carefully consider the implications of these SDLT rules on their budget. Given the complexities and the potential for individual circumstances to affect SDLT liability, seeking advice from a solicitor or financial advisor is recommended. Finally, it is always advisable to stay updated by regularly checking the official UK government websites for any further announcements or changes to SDLT legislation.

Share this on social media

Read the latest articles